The Energy Revolution Will Not Be Subsidized

If asked the question, “Do you think governments should support renewable energy with subsidies?” most progressive trade unionists would probably

Read MoreIf asked the question, “Do you think governments should support renewable energy with subsidies?” most progressive trade unionists would probably

Read More

Caption: Fred Wright cartoon from the 1970s, updated to reflect increases in corporate profits, prices and wages over the past

Read More

Setting the Stage Here in the United States, we have an economic system in which public capital—the publicly issued national

Read More

UPMC Susquehanna closed the former Sunbury Community Hospital on January 31, 2020–about six weeks before the COVID-19 pandemic reached the

Read More

How collective bargaining becomes a revolutionary act.

Read More

You know things have gotten bad for the banking industry when even the bankers themselves are beating up on their

Read More

Recognizing the risks to the public, regulators have begun to step in to curtail abuses and hold accountable those who violate the law in lending practices that affect all borrowers, including those with subprime credit scores. While default rates remain relatively low thus far with these subprime loans, we should guard against complacency. Despite the fact that large banks may be pulling back…

Read More

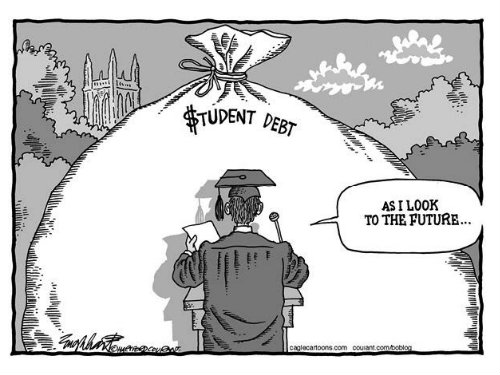

Promising to do something about student debt has become the means for politicians to pretend they are doing something for the 99 percent. That was true even before the 2016 election campaign really got underway. Obama, after all, promised two free years of community college in his 2015 State of the Union address. That idea, like so many others from Republicans and Democrats, did not go anywhere, even though the most recent re-authorization of the 1965 Higher Education Act (HEA) expired in 2013. However, inaction is not just a symptom of Washington gridlock. The reality is that paying for college is a confounding, sprawling sector of the economy involving loans, grants, scholarships, and tax credits.

Read More