Fueling Financialization: The Economic Consequences of Funded Pensions

Figure 1. Composition of U.S. Pension Fund Assets, 1945-2020. Marginal categories excluded for readability are money market fund shares, deposits and currency, and loans. The main component of “Total miscellaneous assets” are claims on the pension plan sponsor. The data include private pension funds, state and local government employee retirement funds, and federal government retirement funds. IRA assets are not included.

The financial sector, whether measured by its total assets or its value-added share of gross domestic product (GDP), has never been a more formidable force in the U.S. economy. The upswing in financialization since the 1970s has coincided with the steady accumulation of long-term retirement savings and their consolidation in institutional capital pools. Pension fund demand for high-field, long-term financial claims has acted as a catalyst for financialization, understood as the reorganization of ownership relations and economic activity in ways that serve the needs of institutional capital pools. In the driver’s seat of this reorganization sits a financial sector whose primary function has shifted from financing investment to preserving wealth, along with a shift in institutional form from banks to asset managers. Under this “asset manager capitalism,” the dominant figures on Wall Street are no longer the CEOs of the big banks but figures such as Larry Fink or Stephen Schwarzman, the CEOs of BlackRock and Blackstone, respectively. Asset managers’ power is most visible vis-à-vis listed corporations—that is, in corporate governance—but it reaches much further. Closely held companies, residential real estate, infrastructure, land—there is no sector that asset managers have not made accessible for financial capital and where they do not exercise substantial structural power, often through outright control.[1]

For labor, the consequences of financialization and the rise of asset manager capitalism have been dire. Countless empirical studies have documented correlations between various measures of financialization, such as payouts to shareholders, and various measures of income and wealth inequality, such as wages.[2] At the same time, ever since Peter Drucker’s warning of the coming of “pension fund socialism” was countered by Jeremy Rifkin and Randy Barber’s positive vision of labor’s capital as an instrument of labor power, the latter has gripped the imagination of scholars and labor organizers.[3] Indeed, the past two decades have seen an impressive increase in pro-worker activism by public-sector and multi-employer, collectively bargained plans known as Taft-Hartley pension funds, and a lively debate is taking place about the prospects for “capital stewardship” to deliver results for U.S. workers.[4] In this context, I argue that the ongoing debate about meso-level prospects for labor’s capital under-appreciates the macro-level consequences of U.S. funded pensions as the world’s single most consequential financializing force over the past half-century.

Standing at $35 trillion in 2021. . .U.S. pension assets account for 62 percent of global pension assets. This money has fueled the growth of the asset management sector . . .

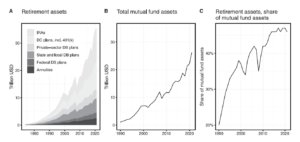

Figure 2. Retirement assets and their importance for the mutual fund sector.

Source. Investment Company Institute, U.S. Retirement Market, second quarter 2021.

Note. Roughly, one-third of total retirement assets are invested in mutual fund shares. Panel C shows that that third accounts for more than 50 percent of the mutual fund sector’s assets under management. DC = defined contribution; DB = defined benefit.

My intention is not to blame global financialization on U.S. labor. The rise of funded pensions is a multi-causal, global phenomenon.[5] Rather, my purpose is to place funded pension systems and their institutional capital pools where they belong—at the center of the history of financialization and asset manager capitalism. Standing at $35 trillion in 2021 (see Figure 2, panel A), U.S. pension assets account for 62 percent of global pension assets.[6] For almost half a century, this money has fueled the growth of the asset management sector, which in many countries has actively lobbied for pension privatization.[7] When pension fund activism brought corporate governance reform, corporations’ quest for shareholder value brought workplace fissuring and wage stagnation.[8] When pension funds pushed into real estate assets for better returns, private equity firms delivered by raising rents and evicting those that could not pay.[9]

The argument is thus directed not against specific pension fund investment practices but against funded pensions tout court. The alternative is a pay-as-you-go (PAYGO) system that redistributes money from the young to the old, at a fraction of the cost of the pension-asset-management complex, and without demand-depressing, financializing consequences. This alternative may seem utopian today. However, creating the conditions for labor-friendly stewardship of labor’s capital is just as ambitious a project. Short of a Promethean overhaul of the macro-financial architecture—think re-regulation and public banking—labor-friendly capital stewardship is bound to remain a Sisyphean task.[10]

Financialization

Financialization in the United States has been explained as the result of the exhaustion of the Fordist growth model. Competition in international trade, de-industrialization, and disinflationary policies all put pressure on political actors to liberalize finance so that newly created credit could substitute for stagnating wage income and sustain aggregated demand.[11] However, as historians Fernand Braudel and Giovanni Arrighi have argued, financialization has been a recurring feature of capitalist development. It tends to be driven by a slowdown of accumulation that makes reinvesting profits in immobile productive capital relatively less attractive to capitalists, who instead seek returns from liquid financial claims.[12] Taking as given a certain level of national income, there are three scenarios under which households will want to increase their savings rate. The first scenario is demographic change. The combination of increasing life expectancy and declining birthrates causes people to set aside more money today, partly because their post-retirement life will be longer, partly because slowing population growth depresses yields.[13] The second scenario is income concentration. Since the wealthy consume a smaller share of their income, channeling more income their way increases desired savings.[14] The third scenario encompasses policies that force households to save more. The single most consequential such policy is a funded pension regime.[15]

The past half-century has been a perfect storm. Societies across the world have grown older and more unequal. At the same time, and often in reaction to the pressures demographic and economic stagnation have placed on states’ redistributive capacity, the capitalization and privatization of pension systems have proliferated.[16] The resulting increase in long-term household savings has fueled the search for yield and the growth of the asset management sector—two core aspects of financialization.

Funded Pensions and Financialization: Two Sides of the Same Coin

Among the thorny issues discussed in the vast literature on the U.S. pension system are the degree to which labor can control its capital, the possibilities for using its control toward progressive ends, and the individualization of risk that comes with defined contribution plans.[17] What is often lost in those debates, however, are the broader economic and financial consequences of what some scholars have called “pension fund capitalism.”[18] Rather than asking how labor can better wield what legal scholar David Webber has dubbed its “last best weapon,” this essay examines the structural forces that tend to make this weapon misfire.

When pension funds pushed into real estate assets for better returns, private equity firms delivered by raising rents and evicting those that could not pay.

In principle, pension funds can be a source of long-term capital serving the local economy, and they have historically played that role. Social scientists Michael McCarthy, Ville-Pekka Sorsa, and Natascha van der Zwan have detailed what “patient” pension capital looks like in practice, listing “the provision of financing for long-term business operations; economically targeted long-term investment; passive ‘anchor’ ownership; and active corporate engagement.”[19] They also argue, convincingly, that pension funds cannot be ascribed investment preferences independently of the meso-level institutional conditions under which they operate, namely, pension fund financing needs, governance capacities, and financial regulations set by the government.[20]

Where there are large institutional capital pools . . . there tend to be structural pressures that compel these actors to “push the envelope of existing investment norms.

What is missing from this analysis, however, is the macro-level. Here, the institutional conditions for pension capital to be patient are the same as the institutional conditions for patient financial capital more generally. In the United States and elsewhere, these conditions prevailed during the three decades following World War II. As noted by the historian Jonathan Levy, during this “age of control,” the United States succeeded in “inducing, but never coercing, capital to fix and settle on the ground, long term, within national territories.”[21] Perhaps not surprisingly, by the mid-1970s, the managers of institutional capital pools became key actors in overturning the conditions of such (soft) financial repression. Where there are large institutional capital pools—be they sovereign wealth, endowment, or pension funds—there tend to be structural pressures that compel these actors to “push the envelope of existing investment norms.”[22] Critics of pension fund capitalism have long argued that rather than financing entrepreneurs and fostering growth, pension money has “[inflated] capital markets in which unproductive takeover and corporate restructuring activity flourishes, while industrial production and employment activity stagnate.”[23] At the same time, their capital feeds an asset management sector geared toward capitalizing on ever-increasing share of economic activity, thus expanding the universe of investable assets.

The need to push the envelope is hard-wired into the U.S. funded pension system, and the reasons run deeper than financing needs or plan design. As pointed out by economic historian Avner Offer, it is “never noticed” by advocates of market provision “that financial markets are not large enough to support welfare transfers.”[24] Invariably, therefore, the supply of pension savings in search of investment outstrips demand for financing from the non-financial sector (firms, households, government). This mismatch means that pension capital contributes to asset price inflation and to declining yields in established, “conservative” asset classes, which in turn gives pension funds a strong incentive to lobby state and federal governments to allow them to move into high-risk investment strategies and asset classes. In this effort, they will invariably be supported by the asset management sector.

Once state governments gave in to pension trustees’ demands to open high-yielding corporate securities to investment by pension funds, fiscal mutualism quickly went out the window.

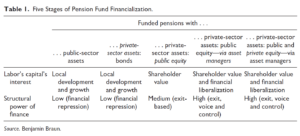

This theory of “pushing the envelope” helps explain the historical trajectory of pension funds’ asset composition. As depicted in the top row of Table 1 (to be read from left to right), pension funds’ asset composition has steadily moved from public, local, and development-oriented investments to more private, global, and predatory investments. To some extent, this movement simply reflects financial liberalization and innovation over the course of the postwar period. At the same time, however, pension capital was a major driver of that liberalization and innovation. Throughout this period, it was far and away the largest institutional capital pool that fueled the growth of mutual, private equity, and hedge funds—in other words, of asset manager capitalism.

Pension Fund Assets: From Public and Local to Private and Global

The macro-financial regime of the postwar period was characterized by substantial financial repression. Strict financial regulation and controls on international capital mobility subordinated private finance to the interests of the non-financial and the public sectors. To the extent funded pension systems existed, they were “characterized by a close proximity between the state and pension funds.”[25] Accordingly, U.S. public pension funds held assets issued by the public sector, namely, treasuries and municipal bonds (see Figure 1 on opening page). In what historians Michael Glass and Sean Vanatta have aptly named “fiscal mutualism,” New York public pension funds financed the construction of suburban schools (among other public infrastructure projects) by purchasing school district bonds at below-market yields (thereby financing white flight from New York City).[26]

Once state governments gave in to pension trustees’ demands to open high-yielding corporate securities to investment by pension funds, fiscal mutualism quickly went out the window. It gave way to a regime under which pension funds invested in securities issued by private corporations—bonds at first, then increasingly, and eventually predominantly, equities (see figure 1, the opening graphic of this article). When, during the 1970s, the U.S. economy confronted increasing international competition, pension savings were heralded as a crucial source of “patient capital”—capital willing to support U.S. corporations in developing long-term strategies to match those of their competitors from corporatist Germany and Japan. However, as the shift into corporate equities accelerated over the course of the 1980s and 1990s, U.S. pension funds came to be categorized as the paradigmatic “impatient” investors whose power in the realm of corporate governance rested primarily in their ability to (threaten to) exit individual holdings.[27]

. . . [A]rguably [the] most controversial contribution of labor’s capital to the growth of asset manager capitalism has been its push into alternative asset classes.

The shift in pension fund investment from public to private assets is well documented, but the drive to “push the envelope” in the search for risk-adjusted return has since continued. The first step was the delegation of investment to external asset managers. Reliance on asset managers, which began as early as the move into equities in the 1960s, accelerated in the 1980s in the wake of the Employee Retirement Income Security Act of 1974 (ERISA), which imposed new “prudent man” and portfolio diversification requirements. Delegation to asset managers continued to increase throughout the 1990s and 2000s.[28]

By delegating portfolio management, pension funds have handed much of the power associated with stock ownership over to asset managers, whose interests are not generally aligned with those of labor’s capital. Unlike pension funds, whose principals are somewhat ambiguous about the distribution of income between capital and labor—their beneficiaries are recipients of wage income today and capital income tomorrow—for-profit asset managers are in the business, first and foremost, of maximizing their own assets under management. This translates into a pursuit of shareholder value in the case of actively investing asset managers and an overall preference for high asset valuations. Delegation thus adds an investor-asset manager agency problem to the classic shareholder-manager agency problem—the interests of asset managers are not aligned with those of pension fund beneficiaries.[29]

The importance of labor’s capital for the growth of the mutual fund industry cannot be overstated. Figure 2, Panel A, shows the spectacular growth of total retirement assets, from $370 billion in 1974 to $35 trillion in 2021. Of the six main categories, individual retirement accounts (IRAs) and defined contribution plans (including 401(k)s) have seen the fastest growth in recent years. Panel B shows the growth of mutual fund assets, from $1 trillion in 1990 to $26 trillion in 2021. Panel C shows the extent to which the growth of mutual funds has been fueled by retirement assets, whose share in total mutual assets is up from 20 percent in 1990 to more than 50 percent in 2021.

The growth of mutual funds in general, and of providers of exchange-traded funds in particular—notably the three giants BlackRock, Vanguard, and State Street—has turned U.S. corporate share ownership and corporate governance upside down. Asset manager capitalism constitutes a distinct corporate governance regime, characterized by concentrated, yet diversified, shareholdings by for-profit asset management companies with fee-based business models, with little interest in the economic performance of individual portfolio firms.[30]

. . . [L]abor’s capital [has become] a major protagonist in a radical transformation of residential real estate into an asset class for institutional capital pools . . .

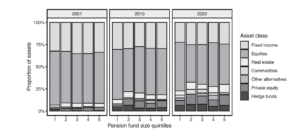

Figure 3. Asset allocation of U.S. public pension funds.

Source. Public Plans Data. Center for Retirement Research at Boston College, Center for State and Local Government Excellence, and National Association of State Retirement Administrators, 2021.

Note. Cash holdings—which are small and invariant—are excluded for readability.

The most recent, and arguably most controversial, contribution of labor’s capital to the growth of asset manager capitalism has been its push into alternative asset classes. In addition to seeking direct exposure to real estate and commodity assets, public pension funds in particular have shifted large amounts of money into private equity and hedge funds. Figure 3 plots this shift using data from 210 state and local pension plans (accounting for 95 percent of state and local plan assets), divided into size quintiles. It shows that across size groups, public pension funds have roughly tripled their alternatives share, from under 10 percent in 2001 to 30 percent in 2020. As in the case of the end of fiscal mutualism in the 1960s, public pension funds’ move into hedge funds was not preordained but required regulatory action. Up until 1996, hedge funds were prohibited from doing business with entities that had fewer than one hundred shareholders. Congress eliminated this rule with the National Securities Markets Improvement Act of 1996, thus opening hedge funds to pension fund trustees.[31] Private equity funds have attracted even more public pension plan capital than hedge funds. They channel this money into leveraged buyouts, whose profitability has long been known to be achieved at the expense of worker wages, health, and safety. Private equity firms have also increasingly invested in real estate assets across the world, making labor’s capital a major protagonist in a radical transformation of residential real estate into an asset class for institutional capital pools.[32] For example, among the eight investors in the Blackstone Property Partners Europe fund, which invests in various types of real estate assets across Europe, the two largest—committing $750 and $470 billion, respectively—are the California Public Employees’ Retirement System (CalPERS) and the California State Teachers’ Retirement System.[33]

To Make Things Better for Labor, Make Them Worse for Labor’s Capital

Today, asset managers rule supreme in the economy. Mutual and exchange-traded fund giants such as BlackRock and Vanguard dominate corporate governance, while private equity firms gobble up everything from elderly care homes to single-family houses. The fodder on which these asset managers have grown so bulky was labor’s capital, and much of the power they wield as shareholders has been won by pension fund activists. Business scholar Richard Marens’ “ironic conclusion” is therefore correct—pension fund activism has done “more to assist the investment community than the American labor movement.”[34] This conclusion may be ironic, but it is not surprising. The reason the hopes of Barber and Rifkin have not been fulfilled is that financial capital earmarked for pensions is still financial capital in search of return, structurally geared toward “pushing the envelope” in terms of investment practices, asset classes, and financial liberalization.

. . .[P]ension fund activism has done “more to assist the investment community than the American labor movement.”

The 35-trillion-dollar question, then, is whether a viable path back to a version of the fiscal mutualism of the early 1960s exists. As governments across the world are looking to finance the economic and technological transformations necessary for decarbonization, this question could not be more urgent. Can labor’s capital provide long-term patient capital for public and private, but primarily local, development-oriented, and green investment projects? The answer is yes, such a path exists, but it is rockier than the Barber-Rifkin tradition has been ready to acknowledge. In a system in which financial return is structurally linked to predation, exercising labor power through capital stewardship is doomed to fail. Unlocking the progressive promise of labor’s capital requires a macro-financial regime that strictly regulates finance and that allows for greater economic democracy. The public would play a much greater role in credit creation and allocation, labor’s capital would be uncoupled from the for-profit asset management sector, and employee equity funds and other forms of mutual ownership would institutionalize profit-sharing and co-determination at the firm level.[35] On the transition path to such a “real utopia,” funded pensions appear as an obstacle rather than a stepping stone because they create a sequencing problem—things would have to get worse for labor’s capital before they get better for labor.

Acknowledgments

I would like to thank Philipp Golka, Sanford Jacoby, Sean Vanatta, and Natascha van der Zwan, as well as the editors, for their time and their constructive comments an an earlier draft of this essay.

Notes

1. Benjamin Braun, “From Exit to Control: The Structural Power of Finance under Asset Manager Capitalism,” SocArXiv, 2021, https://osf.io/preprints/socarxiv/4uesc.

2. Ken-Hou Lin and Donald Tomaskovic-Devey, “Financialization and U.S. Income Inequality, 1970-2008,” American Journal of Sociology 118, no. 5 (2013): 1284-329; Lenore Palladino, “Financialization at Work: Shareholder Primacy and Stagnant Wages in the United States,” Competition & Change 25 (2021): 382-400; Ignacio Alvarez, “Financialization, Non-Financial Corporations and Income Inequality: The Case of France,” Socio-Economic Review 3, no. 3 (2015): 449-75, doi:10.1093/ser/mwv007.

3. Peter F. Drucker, The Unseen Revolution: How Pension Fund Socialism Came to America (New York: Harper & Row, 1976); Jeremy Rifkin and Randy Barber, The North Will Rise Again: Pensions, Politics and Power in the 1980s (Boston, MA: Beacon Press, 1978).

4. Patrick Dixon, “Capital Strategies for the Common Good: A Tool for Labor’s Revival,” New Labor Forum 30, no. 1 (2021): 60-68, doi:10.1177/1095796020983010; David Webber, The Rise of the Working-Class Shareholder: Labor’s Last Best Weapon (Cambridge, MA: Harvard University Press, 2018); Larry Liu and Adam Goldstein, “Labor’s Capital and Worker Well-Being: Do US Pension

Funds Benefit Labor Interests?” Social Forces, no. soab025 (March 31, 2021), doi:10.1093/ sf/soab025; Richard Marens, “Waiting for the North to Rise: Revisiting Barber and Rifkin after a Generation of Union Financial Activism in the US,” Journal of Business Ethics 52, no. 1 (2004): 109-23.

5. On pension financialization, see, for example, Natascha van der Zwan, “Financialisation and the Pension System: Lessons from the United States and the Netherlands,” Journal of Modern

European History 15, no. 4 (2017): 554-84. For recent comparative studies, see Marek Naczyk, “When Finance Captures Labor’s Capital: Dominant Personal Pensions, Resurgent Occupational Provision in Central and Eastern Europe,” Social Policy & Administration 52, no. 2 (2018): 549-62, doi:10.1111/spol.12383; Tobias Wiß, “Reinforcement of Pension Financialisation as a Response to Financial Crises in Germany, the Netherlands and the United Kingdom,” Journal of European Public Policy 26, no. 4 (2019): 501-20; Natascha van der Zwan, “Modelos de Financiarización de

Las Pensiones En Cuatro Estados de Bienestar Europeos,” Revista Internacional de Sociología 78, no. 4 (December 15, 2020): e175, doi:10.3989/ris.2020.78.4.m20.007.

6. Thinking Ahead Institute, “Global Pension Assets Study 2021,” 2021, https://www.thinkingaheadinstitute.org/research-papers/global-pension-assets-study-2021/.

7. Marek Naczyk, “Agents of Privatization? Business Groups and the Rise of Pension Funds in Continental Europe,” Socio-Economic Review 11, no. 3 (01 2013): 441-69, doi:10.1093/ser/mws012; Nils Röper, “Capitalists against Financialization: The Battle over German Pension Funds,” Competition & Change 25, no. 3-4 (July 1, 2021): 428-52, doi:10.1177/1024529421993005.

8. David Weil, The Fissured Workplace (Cambridge, MA: Harvard University Press, 2014).

9. Brett Christophers, “How and Why U.S. Single-Family Housing Became an Investor Asset Class,” Journal of Urban History, Advance online publication (2021).

10. See Robert C. Hockett, “Labor’s Capital: Why and How to Put Public Capital at the Service of Labor,” New Labor Forum 30, no. 1 (2021): 20-31, doi:10.1177/1095796020983317; Daniela Gabor, “Critical Macro-Finance: A Theoretical Lens,” Finance and Society 6, no. 1 (2020): 45-55.

11. Greta R. Krippner, Capitalizing on Crisis. The Political Origins of the Rise of Finance (Cambridge, MA: Harvard University Press, 2011).

12. As does the political economy literature, historians of the longue durée of capitalism point to the exhaustion of a previously successful economic model as chief catalyst of financialization.

However, unlike the political economy literature, the work of historians such as Braudel, Arrighi, and Bas van Bavel shifts from the demand for, to the supply of, financial capital as the driving force of financialization.

13. Adrien Auclert, Hannes Malmberg, Frederic Martenet and Matthew Rognlie, “Demographics, Wealth, and Global Imbalances in the Twenty-First Century,” National Bureau of Economic

Research, 2021.

14. Atif Mian, Ludwig Straub, and Amir Sufi, “What Explains the Decline in R*? Rising Income Inequality versus Demographic Shifts,” 2021, https://www.kansascityfed.org/documents/

8337/JH_paper_Sufi_3.pdf.

15. It is worth noting that pay-as-you-go systems are macroeconomically equivalent to funded pensions in that the value of retirement claims depends on the size of the economy at the point of retirement.

16. See, for example, Sarah M. Brooks, “Interdependent and Domestic Foundations of Policy Change: The Diffusion of Pension Privatization Around the World,” International Studies Quarterly 49, no. 2 (2005): 273-94, doi:10.1111/j.0020-8833.2005.00345.x.

17. Michael A. McCarthy, Dismantling Solidarity: Capitalist Politics and American Pensions Since the New Deal (Ithaca, NY: Cornell University Press, 2017); Webber, The Rise of the Working-Class Shareholder; Jacob S. Hacker, The Great Risk Shift: The New Economic Insecurity and the Decline of the American Dream, rev. 2nd ed. (New York: Oxford University Press, 2019); Liu and Goldstein, “Labor’s Capital and Worker Well-Being”; Sanford M. Jacoby, Labor in the Age of Finance: Pensions, Politics, and Corporations from Deindustrialization to Dodd-Frank (Princeton: Princeton University Press, 2021).

18. See, for example, Jan Toporowski, The End of Finance: Capital Market Inflation, Financial Derivatives and Pension Fund Capitalism (London: Routledge, 2000); Adam D. Dixon, “The Rise of Pension Fund Capitalism in Europe: An Unseen Revolution?” New Political Economy 13, no. 3 (2008): 249-70, doi:10.1080/13563460802302560; Gordon L. Clark, Pension Fund Capitalism (Oxford:

Oxford University Press, 2000); Dirk Bezemer, “Pension Fund Capitalism: A Case Study of the Netherlands,” IMK Working Paper (Duesseldorf: Hans Boeckler Foundation, forthcoming).

19. Michael A. McCarthy, Ville-Pekka Sorsa, and Natascha van der Zwan, “Investment Preferences and Patient Capital: Financing, Governance, and Regulation in Pension Fund Capitalism,” Socio-Economic Review 14, no. 4 (2016): 753-69.

20. McCarthy et al., “Investment Preferences and Patient Capital,” 754. 21. Jonathan Levy, Ages of American Capitalism: A History of the United States (New York: Random House, 2021), 396.

22. Ewald Engelen, “The Logic of Funding European Pension Restructuring and the Dangers of Financialisation,” Environment and Planning A 35, no. 8 (2003): 1366.

23. Toporowski, The End of Finance, 53.

24. Avner Offer, “The Market Turn: From Social Democracy to Market Liberalism,” The Economic History Review 70, no. 4 (2017): 1055.

25. van der Zwan, “Financialisation and the Pension System Lessons from the United States and the Netherlands,” 577.

26. Michael R. Glass and Sean H. Vanatta, “The Frail Bonds of Liberalism: Pensions, Schools, and the Unraveling of Fiscal Mutualism in Postwar New York,” Capitalism: A Journal of History and Economics 2, no. 2 (2021): 427-72.

27. Peter A. Hall and David Soskice, “An Introduction to Varieties of Capitalism,” in Varieties of Capitalism. The Institutional Foundations of Comparative Advantage, ed. Peter A. Hall and David Soskice (Oxford: Oxford University Press, 2001), 1-68.

28. On the consequences ERISA, see Sabine Montagne, “Investing Prudently: How Financialization Puts a Legal Standard to Use,” Sociologie du Travail 55, no. Supplement 1 (2013): 48-66; van der Zwan, “Financialisation and the Pension System: Lessons from the United States and the Netherlands,” 566.

29. See, for example, Lucian A. Bebchuk, Alma Cohen, and Scott Hirst, “The Agency Problems of Institutional Investors,” Journal of Economic Perspectives 31, no. 3 (2017): 89-102.

30. Benjamin Braun, “Asset Manager Capitalism as a Corporate Governance Regime,” in The American Political Economy: Politics, Markets, and Power, ed. Jacob Hacker, Alexander Hertel-Fernandez, Paul Pierson, Kathleen Thelen (Cambridge: Cambridge University Press, 2021), https://osf.io/preprints/socarxiv/v6gue/.

31. Webber, The Rise of the Working-Class Shareholder, 84.

32. Brett Christophers, “Mind the Rent Gap: Blackstone, Housing Investment and the Reordering of Urban Rent Surfaces,” Urban Studies, Advance online publication (August 11, 2021); Desiree Fields and Sabina Uffer, “The Financialisation of Rental Housing: A Comparative Analysis of New York City and Berlin,” Urban Studies 53, no. 7 (2016): 1486-502; Daniela Gabor and Sebastian Kohl, “MyHome Is an Asset Class: The Financialization of Housing in Europe” (Report for the Greens/European Free Alliance in the European Parliament, forthcoming.

33. Gabor and Kohl, “My Home Is an Asset Class,” 42.

34. Marens, “Waiting for the North to Rise,” 109. He further notes (p. 10) that pension fund initiatives “have helped loosen the investment constraints imposed on financial fiduciaries” and

“make it easier for other shareholder activists to communicate with each other and to confront, and even effectively oppose, corporate management.”

35. On employee equity funds, see Lenore Palladino, “The Potential Benefits of Employee Equity Funds in the United States,” Journal of Participation and Employee Ownership, Advance online publication 2021. On democracy at the firm level, see Isabelle Ferreras, Firms as Political Entities: Saving Democracy through Economic Bicameralism (Cambridge: Cambridge University Press, 2017).

Author’s Biography

Benjamin Braun is a senior researcher at the Max Planck Institute for the Study of Societies in Cologne, Germany. His current research focuses on the political economy of asset manager capitalism. His work has been published, among others, in New Political Economy, Review of International Political Economy, and Socio-Economic Review.