Who Pays for Inflation?

Caption: Fred Wright cartoon from the 1970s, updated to reflect increases in corporate profits, prices and wages over the past year.

As of mid-2022, it is clear that inflation has become the Biden administration’s greatest liability. Rising prices have undermined what has otherwise been a strong recovery from the depths of the pandemic, as steady nominal wage growth has failed to keep up with elevated costs. By April 2022, the Consumer Price Index (CPI) was 8.3 percent higher than the year prior, the greatest twelve-month increase in forty years. The expenses that bear most acutely on working-class households were all rising fast—housing was up 5 percent, food more than 9 percent, and energy some 30 percent.[1] Politically, the first casualty was Build Back Better, which Senators Joe Manchin and Kyrsten Sinema opposed, at least publicly, on account of its inflationary potential. The war in Ukraine, which sent energy prices soaring, only aggravated the problem. Whatever happens to the course of prices in the months to come—and at this point, it would be foolish to hazard any predictions—the issue has already worked to the Democrats’ disadvantage as we approach the November midterms. So much for the historic opportunity afforded by the surprise outcome in the 2020-2021 Georgia senate run-off election.

Biden’s critics, of course, have had no trouble placing the blame squarely on the economic policy response to the pandemic. The American Rescue Plan, together with the Coronavirus Aid, Relief, and Economic Security (CARES) Act passed under Trump’s watch, provided much-needed relief and in fact enabled millions of households to emerge from the pandemic more economically secure. But as figures like Larry Summers—an architect of Democratic neoliberalism—saw it, this fiscal stimulus overheated the economy, producing a level of demand well in excess of the capacity available to absorb it. Workers’ improved bargaining position, moreover, resulted in a labor shortage that threatened to ignite a dangerous “wage-price spiral.” To get the situation under control, Summers and others have called for the textbook response to a hot economy: namely, to cool it down through tighter monetary policy and limits on further federal spending, measures that are intended to raise unemployment and perhaps invite a recession. Better to take that medicine now, they argue, than to endure more painful consequences down the road. Although Federal Reserve Chair Jerome Powell displayed caution against overreacting for much of 2021, by the end of the year he had come around to this argument and announced the steepest schedule of interest rate hikes since 2000.

But if strong demand has contributed to the inflation, as some progressive economists have admitted may be the case, the real source of the pressure has been constrained supply. Never before had the global economy been intentionally shut down, as it was during the peak of the Covid-19 pandemic, and the process of restarting it was bound to be accompanied by various frictions that led to the shortages and bottlenecks which have cascaded along the intricate supply chains spanning the entire world. The global crunch in semiconductors, a key input into all manner of electronic devices, was only the most publicized example of this phenomenon. What’s more, insofar as demand has been a factor, the issue has not been the aggregate volume of consumer spending but its composition.[2]

Through the pandemic, people were buying more things and utilizing fewer services—notably in the restaurant and tourism sectors. The result was that inflation was for the past year confined almost entirely to durable goods, above all vehicles. Supply problems were supposed to subside, a presumption that led many, Powell included, to believe that inflation would prove to be “transitory.” That, clearly, has not been the case, and the Ukraine war and the renewed lockdowns in China suggest that supply-side inflation may persist for some time to come. Even more ominously, climate change, together with ongoing geopolitical tensions, could well make supply-side inflation a permanent feature of the global capitalist landscape.[3]

. . . [A]n orthodox anti-inflation policy . . . forecloses avenues toward the public investment needed to address the major crises of our time, particularly the climate crisis.

Tighter monetary policy—namely, interest rate hikes—can do nothing to get at these underlying supply problems, and indeed it could just make the situation worse by slowing the economy as prices continue to rise—the dreaded outcome of “stagflation,” or simultaneously rising unemployment and persisting inflation. In addition to the immediate effect of higher interest rates, an orthodox anti-inflation policy presents a larger, structural dilemma for working-class politics: It forecloses avenues toward the public investment needed to address the major crises of our time, particularly the climate crisis. Building green infrastructure, developing alternative energy sources, and expanding public goods—like care, education, and housing—require substantial and sustained federal expenditure. Over time, such investment may enhance the economy’s productive capacity and thereby mitigate the supply-side inflation we are now experiencing. But all else equal, in the short term, an economic policy of this sort would produce a level of demand that generates inflation. A revitalized labor movement able to raise wages on a national level could also be an inflationary factor.

In short, it is important to admit that the things we want and need do bring the risk of inflation. This is because a favorable labor market, and the working-class struggle it enables, produces competition over claims on total income, a dynamic that is transmitted in the form of inflation—higher wages could eat into profits, or they could be passed on in the form of higher prices. As the economist Joan Robinson once put it, inflation is an expression of the “class war.”[4] Viewed from another angle, controlling inflation requires state management of these competing claims. In recent decades, that management has taken the form of suppressing working-class wage growth. This is what restrictive monetary policy and budgetary restraint is about—it is an incomes policy, but one that functions in the interest of the ruling class. For a working-class politics to get through the barrier of inflation, it must confront this fundamental distributional problem and achieve a different, more egalitarian incomes policy.

Pro-Labor Inflation Control?

This dilemma raises the question of whether there are alternative means of dealing with the problem of inflation. Recently, progressive economists and activists have proposed improved antitrust enforcement, a temporary excess profits tax, and price controls as possible solutions. All begin from the premise that rising prices have been accompanied by record corporate profit margins, and they therefore represent an important effort to shift the terms of debate away from an exclusive focus on wages. This is not to say that corporate price-gouging is the cause of the current inflation. The market power of organized business is not significantly greater today than it was a decade ago, when consumer prices were stable. Rather, as Josh Bivens of the Economic Policy Institute has demonstrated, the pandemic-related supply problems have created an environment in which firms with sufficient power have exercised it through raising prices rather than suppressing wages, as they had done in decades past. Put another way, they are spreading and intensifying an inflation that originated elsewhere.[5] In any event, whatever caused inflation in the first place, the issue now is how it will be controlled. That is, who will bear the burden of policies aimed at reducing the price level—labor or capital? The virtue of these proposals is that they raise that question.

Let’s start with antitrust. The Biden administration has argued that the lack of competition in the shipping industry, for instance, has worsened the price pressures that originated in disrupted global supply chains.[6] In other areas, like pharmaceuticals, the high prices set by firms with control over supply take a toll on working-class budgets even if they do not register in the aggregate inflation data, as prescription drugs account for less than 1 percent of the CPI.[7] Antitrust enforcement, or even the threat of it, may well encourage such corporations to consider the public interest in determining what to charge. But antitrust works slowly, through lengthy litigation, and it is unlikely to have appreciable effects in the short term. More significantly, increased competition—which often drives down prices and wages—does not always have beneficial employment effects, as workers in industries ranging from garment production in the past to nail salons today can attest.

. . . [I]t is important to admit that the things we want and need do bring the risk of inflation.

What about a windfall profits tax or price controls? A windfall profits tax may be more effective at targeting the issue of monopoly power and price gouging. During World War II, a 95 percent windfall profits tax was imposed on returns above a specified level, and Senator Bernie Sanders has introduced legislation modeled on that example to deter corporate price gouging over the next few years. As an emergency measure aimed at limiting the degree to which market power is serving as a channel for propagating inflationary pressure, this could be a valuable tool. There are even more extensive precedents for price controls.[8] For most of the twentieth century, prices in the transportation industry—railroads, trucking, and airlines—were subject to oversight by different regulatory agencies. Utilities as well as insurance also have a long history of rate regulation. And in certain cities, rent control and stabilization remains an important part of housing policy. More comprehensive price controls have mainly proven to be an effective means of managing inflation and the cost of living during wartime. The classic example here is the World War II–era Office of Price Administration (OPA), which placed ceilings on the price of virtually every good and service in the economy for the duration of the conflict, an effort that successfully kept inflation at bay even as the demands of defense production pushed the economy to the limits of total capacity.[9]

The Federal Reserve campaign against inflation was . . . an offensive against the U.S. labor movement . . .

The fate of the OPA is instructive for thinking through the dilemma facing us today. In the aftermath of the war, the labor movement saw the politics of inflation as inseparable from their broader goals of achieving full employment policy and real improvements in working-class living standards. The process of reconverting to a civilian economy was bound to involve supply frictions that together with pent-up demand from the war and workers’ wage militancy threatened to unleash inflation. To avoid this, unions in the immediate post-war period pressed for the maintenance of the OPA in peacetime and undertook the largest strike wave in U.S. history, led by the United Auto Workers’ (UAW) demand during the strike of 1945-1946 that General Motors grant substantial wage increases without increasing prices. At bottom, this amounted to a campaign for higher wages at the expense of profits and an ongoing role for the state in managing these competing claims on total income. That is, it was about politicizing the question of who gets what.[10]

The UAW’s wage and price demands represented a direct attack on capitalist class prerogatives, but the issue of price control carried larger implications as well. A standard and indeed legitimate criticism of price control is that it distorts the market signals that incentivize production. When prices rise, the reasoning goes, businesses have an interest in capturing potential profits by increasing production accordingly. Suppression of prices and profit margins, in other words, prevents output from meeting demand and thereby produces shortages. This is just what happened in the year after the war, as businesses cut production, leaving store shelves empty and consumers desperate. To avoid this outcome, the state would have had to assume a larger role in directing production and planning investment, likely through socialization of key industries. Taking the financial sector under public control, taxing wealth and high incomes, intervening in labor markets to minimize wage differentials, and restricting certain kinds of consumption would all need to follow. In short, it would have to involve restructuring capitalism as we know it.

. . . [T]he trajectory of interest rates over the past seventy-five years reads something like an index of working-class power.

Accomplishing this would have taken a level of power that, even at its high point in the early post-war years, the U.S. working class did not possess. Organized business waged an aggressive and successful campaign to kill the OPA in 1946, and over the course of that year, the inflation that unionists had feared took off, hitting some 20 percent. In November, the Republicans rode the price wave to a rout at the polls, and together with Southern Democrats, they passed the Taft–Hartley Act over President Truman’s veto the next year. The inflationary context also handed conservatives a ready-made argument against further expansion of the New Deal state: public expenditure guaranteeing jobs and health care for all would only make matters worse. It was here as well that the Federal Reserve, which during the 1930s and 1940s had had its authority subordinated to the spending needs of the federal government, waged a struggle to win independence through the famous 1951 “Accord” with the Treasury Department. As a UAW official commented at the time, the question was whether the central bank would be “a part of our Government” or “a Government apart,” and the answer bears on working-class politics to this day.[11]

For the next three decades, inflation or the specter of it, set the boundary of the politically possible, always placing a brake on the ambitions of Keynesian policies directed at achieving economic expansion and full employment. Unions faced pressure to limit wages to the growth of productivity and sought to protect members’ purchasing power through cost-of-living adjustments. But not everyone had a union. Still, so long as the domestic economy prospered, this arrangement could allow for a broad improvement in living standards. In the absence of a comprehensive political solution to the inflation dilemma, however, organized labor was vulnerable to attack when prices began to climb in the late 1960s and soared in the 1970s. A number of complex factors contributed to this crisis—spending on the war in Vietnam, the devaluation of the dollar following the termination of the Bretton Woods fixed-exchange rate regime, the oil and other commodity price surges, a secular slowdown in productivity, and, indeed, working-class wage militancy.[12] But whatever its causes, a long-term solution could once again only be achieved through a restructuring of the class relations that generated competing claims on a limited total income.

This time, that restructuring was achieved on terms deeply unfavorable to the working class. Under Chair Paul Volcker, the Federal Reserve took to heart Chicago School economist Milton Friedman’s argument that the organized working class, protected by the Keynesian commitment to low unemployment, had raised inflation expectations and allowed a wage-price spiral to set in. To eliminate those expectations, Volcker implemented a draconian monetary policy that took interest rates through the roof and set off a painful recession at home and debt crises across the Global South. The action inaugurated the neoliberal era, and ever since it has served as the cautionary tale of the painful price that must be paid when inflation is allowed to run too high.

The Age of Easy Money

Over the four decades following that Volcker Shock, consumer price inflation was not a serious problem. But, of course, that period was also marked by rising inequality, public-sector retrenchment, and financialization. This correlation is not coincidental. The Federal Reserve campaign against inflation was, again, an offensive against the U.S. labor movement, which central bankers and conservative officials understood as the institutional driver of inflation expectations. Neoliberal policy at home together with trade liberalization and the resultant internationalization of manufacturing consolidated the victories achieved by Volcker and then Ronald Reagan, and the economic insecurity these victories produced deserves most of the credit for the stability in the consumer price level over the past generation.

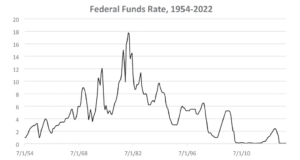

Figure 1. The Federal Funds Rate is the short-term interest rate at which banks borrow from one another.

Figure 1. The Federal Funds Rate is the short-term interest rate at which banks borrow from one another.

Source. Board of Governors of the Federal Reserve System (United States), Federal Funds Effective Rate [FEDFUNDS], retrieved from Federal Reserve Economic Data, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FEDFUNDS, May 26, 2022.

If this monetary regime of low wages, low interest rates, and low consumer price inflation was a boon to the financial sector, it also created the conditions for a more progressive fiscal policy.

Paradoxically, this working-class defeat created the conditions for both the growth of a speculative asset economy and for the Biden administration’s embrace of a new, more expansive fiscal policy. Once inflation had been vanquished, interest rates began a historic, secular decline that may only now be reversing direction. Indeed, the trajectory of interest rates over the past seventy-five years reads something like an index of working-class power. To put it bluntly, monetary authorities concluded that in the absence of a credible working-class threat, inflation was less of a danger, and policy could adjust accordingly. As past Chair of the Federal Reserve Alan Greenspan put it in explaining why inflation failed to materialize during the late 1990s economic boom, “Atypical restraint on compensation increases has been evident for a few years now and appears to be mainly the consequence of greater worker insecurity.” Hindsight affords the benefit of understanding that what then seemed like “atypical restraint”—in comparison with the wage militancy of a couple decades prior—was actually the new normal.

Of course, not everyone exhibited restraint. As capital became cheaper to access, an increasingly unregulated financial sector pushed asset prices to dangerously high levels, a dynamic that contributed to the Great Financial Crisis in 2008. In the wake of the crash, the Federal Reserve under Ben Bernanke adopted what was then an unprecedented monetary policy of ultra-low short-term interest rates and “quantitative easing,” or monthly purchases of bonds intended to bring down long-term borrowing costs and encourage investment. If these measures helped to avert a depression, they also provided the fuel for an incredible asset price boom, one that yet again accrued most of all to the wealthy. It also facilitated the emergence of what political scientist Benjamin Braun has called “asset manager capitalism,” in which colossal firms like BlackRock sit at the apex of the global economy.[13] Notably, though, even as the total monetary base of the national economy swelled almost five-fold between 2010 and 2014, inflation stubbornly refused to budge, averaging less than the Federal Reserve’s conservative 2 percent target over the decade as a whole. This experience suggested that in fact, the danger of recession accompanied by deflation was of greater concern than renewed inflation.

. . . [T]he only force that stands a chance at such a restructuring—or transcending—of capitalism as we know it is an organized working class with a radical political vision.

If this monetary regime of low wages, low interest rates, and low consumer price inflation was a boon to the financial sector, it also created the conditions for a more progressive fiscal policy. Specifically, deficits no longer appeared to be a barrier to public investment, as low borrowing costs promised to enable the federal government to easily finance expenditures over the long-term. This was the context in which the Biden administration formulated its ambitious physical and social infrastructure program. While the fiscally conservative ideological climate still required the administration to demonstrate on paper how the Build Back Better plan would pay for itself in time, in truth there seemed to be no structural obstacle to relying on debt to make it possible. The line separating monetary and fiscal policy had been blurred thanks to the Federal Reserve’s new posture, and this held the promise of a definitive break from the discipline demanded through the neoliberal era. Or as proponents of Modern Monetary Theory (MMT) put it, the only limits on federal spending were political will and the objective physical capacity of the economy.[14] Technically speaking, jobs for all and a Green New Deal were within reach.

If inflation is back, however, the whole calculus might have to change. For one, under a more hawkish Federal Reserve, the possibility of fiscal-monetary coordination directed toward progressive ends may no longer be realistic. And a higher level of public spending, with the inflation-generating demand it creates, may be off the table in any case. In short, the hope of a straightforward and painless path to the robust public investments needed to meet the crises of climate and care has been called into question. There can be no technical macroeconomic solution to these urgent issues that does not reckon with the balance of power in our society; more than anything else, the politics of inflation are a reminder of this fact. Overcoming the inflationary predicament that a more just social, environmental, and economic policy will inevitably raise requires confronting directly the difficult issues of income distribution and investment control, just as it did in the mid-twentieth century. Then as now, the only force that stands a chance at such a restructuring—or transcending—of capitalism as we know it is an organized working class with a radical political vision. It is of some comfort, on that note, that we have seen emerge alongside these new politics of inflation the initial flickers of such a movement.

Notes

1. “Consumer Price Index—April 2022,” available at https://www.bls.gov/news.release/cpi.nr0.htm.

2. See, for example, Hyun Song Shin, “Bottlenecks, Labour Markets, and Inflation in the Wake of the Pandemic,” Bank of International Settlements, December 9, 2021, available at https://www.bis.

org/speeches/sp211209.pdf.

3. For an interesting financial sector perspective on this point, see BlackRock Investment Institute, “A World Shaped by Supply,” January 2022, available at https://www.blackrock.com/corporate/literature/whitepaper/bii-macro-perspectives-january-2022.pdf.

4. Joan Robinson, “The Age of Growth,” Challenge 19, no. 2 (1976): 4-9.

5. Josh Bivens, “Corporate Profits Have Contributed Disproportionately to Inflation. How Should Policymakers Respond?” Working Economics Blog, Economic Policy Institute, April 21, 2022, available at https://www.epi.org/blog/corporate-profits-have-contributed-disproportionately-to-inflation-how-shouldpolicymakers-respond/.

6. David Dayen, “Biden Wants to Take Down the Ocean Shipping Cartel,” The American Prospect, February 28, 2022, available at https://prospect.org/economy/biden-wants-totake-down-the-ocean-shipping-cartel/.

7. The relative weights of goods and services in the CPI can be found here, available at https://www.bls.gov/cpi/tables/relative-importance/home.htm.

8. Excess profit taxes were imposed during World War I, World War II, and the Korean War. More recently, an excess profits tax on oil industry profits was passed in April 1980 after the Carter

administration terminated price control on domestically produced oil. See W. Carl Biven, Carter’s Economy: Policy in an Age of Limits (Chapel Hill: UNC Press, 2002), 163-84.

9. On the Office of Price Administration (OPA), see Meg Jacobs, Pocketbook Politics: Economic Citizenship in Twentieth Century America (Princeton: Princeton University Press, 2004).

10. See Nelson Lichtenstein, “From Corporatism to Collective Bargaining: Organized Labor and the Eclipse of Social Democracy in the Postwar Era,” in The Rise and Fall of the New Deal Order, 1930-1980, ed. Steve Fraser and Gary Gerstle (Princeton: Princeton University Press,1989), passim.

11. Subcommittee on General Credit Control and Debt Management of the Joint Committee on the Economic Report, 82nd Cong., 2nd sess., Hearings before the Subcommittee on General Credit Control and Debt Management (Washington, DC: U.S. Government Printing Office, 1952), 818.

12. In 1944, the Bretton Woods agreement established the structure of the international monetary system for the post-war period, whereby currencies would be set fixed-exchange rates

relative to the dollar, which would be convertible to gold. The arrangement was intended to provide greater flexibility than the old gold standard. The International Monetary Fund and the

World Bank also originated at Bretton Woods. On working-class militancy in this period, see for example, Aaron Brenner and Robert Brenner, Rebel Rank-and-File: Labor Militancy and Revolt from Below (London: Verso, 2020)

13. Benjamin Braun, “Asset Manager Capitalism as a Corporate Governance Regime,” in The American Political Economy: Politics, Markets, and Power, ed. Jacob S. Hacker, Alexander Hertel-Fernandez, Paul Pierson, and Kathleen Thelen (Cambridge: Cambridge University Press, 2021), passim.

14. See, for example, Stephanie Kelton, The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy (New York: Public Affairs, 2020).

Author Biography

Samir Sonti is an assistant professor at the CUNY School of Labor and Urban Studies.